|

Efficiency

and Performance of Conventional and

Islamic Banks in GCC Countries

Lawrence Taii

Correspondence:

Lawrence Tai, PhD, CPA

Professor of Finance

Zayed University

PO Box 144534, Abu Dhabi

United Arab Emirates

Email:

Lawrence.Tai@zu.ac.ae

Abstract

This paper examines the efficiency

and performance of 58 publicly listed

conventional and Islamic national

banks in the Gulf Cooperation Council

(GCC) countries between 2003 and 2011.

A translog cost function is used to

evaluate the efficiency of the GCC

banking sector and multiple regression

analysis is employed to identify factors

affecting the performance of the 58

national banks. Empirical findings

reveal that Masraf Al Rayan of Qatar

(an Islamic bank) was the most efficient

bank while Kuwait Finance House (also

an Islamic bank) was the least efficient

bank during the study period. Conventional

banks were more profitable, liquid,

and solvent than Islamic banks during

the earlier years of the study period

while Islamic banks were more profitable,

liquid, and solvent than conventional

banks during the later years of the

study period. Regression results indicate

that economic conditions, bank size,

financial development, operating costs,

and type of bank (conventional or

Islamic) are significant variables

affecting return on average assets.

Introduction

This paper examines the efficiency

and performance of 58 publicly listed

conventional and Islamic national

banks in the Gulf Cooperation Council

(GCC) countries between 2003 and 2011.

GCC has six member states: Bahrain,

Kuwait, Oman, Qatar, Saudi Arabia,

and the United Arab Emirates (UAE).

The banking sector is crucial to the

development of any economy; it is

also one of the major driving forces

of economic growth in developing countries.

Banks are special financial intermediaries

whose operations are unique in financial

markets and impact strongly on an

economy. Hence, research on efficiency

and performance of the banking sector

has important policy implications.

A higher degree of efficiency and

performance in banking markets is

expected to provide welfare gains

by reducing the prices of financial

services and thereby accelerating

investment and growth.

The objective of this paper is to

study the efficiency and performance

of conventional and Islamic banks

in GCC countries. As commercial banks

play a vital role in the financing

of an economy, banking efficiency

exerts an important impact on a country's

economic development. Bank performance

has been a key issue particularly

in developing countries as commercial

banks are the dominant financial institutions

in these countries and they represent

the major source of financial intermediation.

Evaluating their efficiency and performance

is crucial to depositors, owners,

potential investors, managers, and

regulators.

GCC Economic Review

The GCC is an oil-based economy with

the largest proven crude oil reserves

in the world. This region ranks as

the largest producer as well as exporter

of petroleum. The economies of GCC

countries have been growing very rapidly

during the 2000-2008 period. This

spectacular economic boom came to

a sudden halt in 2009 after the emergence

of the global financial crisis in

late 2008. Growth resumed in 2010.

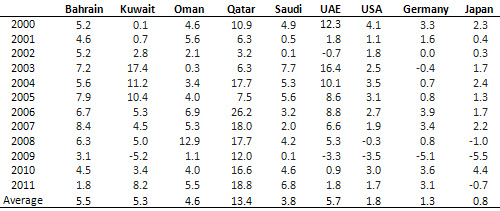

Table 1 displays the real GDP growth

rate for the six GCC members and three

industrialized countries between 2000

and 2011. Compared to the world's

three most industrialized countries,

the GCC economic growth has been very

impressive and all six GCC countries

outperformed the three industrialized

countries. In particular, Qatar's

economic growth has been phenomenal,

with double-digit average growth rate

over this period.

Table 1: Real GDP Growth Rate (%),

2000-2011

Source: Knoema.com

Given the volatility in oil prices,

the GCC countries have realized that

economic diversification is the only

feasible way forward to create long-term,

sustainable growth. They have focused

their development on industries such

as tourism and financial services.

As a result, the GCC banking industry

is gearing up for change in a region

that is accelerating its growth.

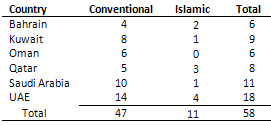

Table 2 shows the number of publicly

listed national banks for each GCC

country at the end of 2011. UAE has

the largest number of conventional

and Islamic banks. There is no Islamic

bank in Oman.

Table 2: Number of Public National

Banks by Country and Type, 2011

Source: Gulfbase.com

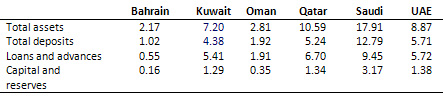

Table 3 presents four selected banking

indicators for GCC banks for 2011.

Saudi Arabian banks have the highest

average total assets, average total

deposits, average loans and advances,

and average capital and reserves,

while Bahraini banks have the lowest.

Table 3: Selected Banking Indicators

(End of 2011 average per bank, in

billions of USD)

Source: Central Bank Statistical Bulletins,

2012.

Literature Review

A large number of studies have been

conducted in measuring efficiency

and performance in the banking industry.

In the literature, two major approaches

have been taken to measure efficiency

in the banking industry: parametric

and nonparametric. Nonparametric approaches

like data envelopment analysis (DEA)

consider the whole distance from the

frontier as inefficiency. These methods

are therefore deterministic as they

do not include the possibility of

measurement errors in the estimation

of the frontier and hence they may

overestimate the inefficiencies. DEA

approach has been used by Ozkan-Gunay

& Tektas (2006) to study the efficiency

of the Turkish banking sector, by

Chang & Chiu (2006) to examine

the efficiency of Taiwan's banking

industry, and by Fitzpatrick &

McQuinn (2005) to investigate the

efficiency of UK and Irish credit

institutions, just to name a few.

Parametric approaches such as the

stochastic frontier approach (SFA)

and the distribution-free approach

(DFA) do not suffer from the above-mentioned

drawback. SFA makes some distributional

assumptions to disaggregate the residual

from the frontier into an inefficiency

term and a random disturbance, which

are arbitrary. SFA has been used by

Inui, Park, & Shin (2008) to study

the comparative efficiency of Japanese

and Korean banking and by Fitzpatrick

& McQuinn (2005) to investigate

the efficiency of UK and Irish credit

institutions. DFA has been proposed

to resolve the major criticism of

the SFA, namely its distributional

assumptions, by adopting more intuitive

assumptions to separate inefficiency

from random disturbance. DFA has been

used by Matousek, R. & Taci, A.

(2004) and by Pruteanu-Podpiera, Weill,

& Schobert (2008) to examine the

efficiency of the Czech banking industry.

Using regression, Al-Tamimi (2010)

investigated the factors affecting

the performance of UAE Islamic and

conventional national banks during

the 1996-2008 period. His results

indicate that liquidity and concentration

were the most significant determinants

of conventional banks' performance

while cost and number of branches

were the most significant determinants

of Islamic banks' performance (measured

by return on assets and return on

equity).

Ika & Abdullah (2011) compared

the financial performance of Islamic

and conventional banks before and

after the enactment of Indonesia's

Islamic Banking Act of 2008. They

found no major difference in the financial

performance between the two types

of banks, except in liquidity where

Islamic banks were generally more

liquid than conventional banks.

Fayed (2013) compared the performance

of Islamic and conventional banks

in Egypt. His findings indicate that

conventional banks dominated Islamic

banks in profitability, liquidity,

credit risk management as well as

solvency.

A number of studies have been conducted

in identifying factors affecting the

performance of Islamic and conventional

banks in Pakistan (Jaffar & Manarvi,

2011; Hanif, Tariq, Tahir, & Momeneen,

2012; Sehrish, Saleem, Yasir, Shehzad,

& Ahmed, 2012; Usman & Khan,

2012). Jaffar & Manarvi found

that Islamic banks performed better

in possessing adequate capital and

better liquidity position while conventional

banks had better performance in management

quality and earnings ability. Hanif,

et al concluded that in terms of profitability

and liquidity conventional banks led,

while in credit risk management and

solvency maintenance Islamic banks

dominated. Sehrish's findings indicate

that Islamic banks were less risky

in terms of dealing in loans and less

efficient in expense management as

compared to conventional banks. Usman

and Khan's results show that Islamic

banks had higher growth rate, profitability,

and liquidity power than conventional

banks.

Previous research were almost exclusively

single country studies that examined

either bank efficiency or performance.

This paper is the first attempt to

investigate the efficiency and performance

of conventional and Islamic national

banks in GCC countries. DFA is applied

to measure efficiency and multiple

regression analysis is used to examine

factors affecting bank performance.

Methodology

This paper has two objectives. The

first objective is to evaluate the

efficiency of the GCC banking sector

during the 2003-2011 period. A translog

cost function is estimated for all

the banks in the sample. Each bank's

efficiency is then computed as the

deviation from the most efficient

bank's intercept term. The second

objective is to determine the factors

affecting the performance of GCC conventional

and Islamic banks.

Measurement of Efficiency: the Distribution-Free

Approach

The distribution-free approach (DFA)

is used to provide evidence on the

level of banking efficiency in the

GCC. Using a fixed-effects model,

inefficiency is estimated from the

value of a bank-specific dummy variable.

The following translog cost function

is estimated for all the banks in

the sample:

The above translog cost function has

one output (loans, y) and three input

prices (labor, physical capital, and

borrowed funds). The price of labor

is measured by the ratio of personnel

expenses to total assets (w1).

The price of physical capital is defined

as the expenses for physical capital

to fixed assets (w2).

The price of borrowed funds is defined

as the ratio of interest expense to

borrowed funds (w3).

The DFA approach is applied and it

is assumed that the difference in

the actual and predicted cost for

a given cross-sectional period is

a combination of persistent inefficiency

component and a random component (Berger,

1993). It is possible to obtain the

persistent inefficiency component

by averaging out these differences

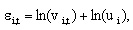

over time. Following Hunter and Timme

(1995), the error term bank i in time

t can be expressed as:

where ln(vi,t) is a random error component

that varies with time and is distributed

with a zero mean over time, and ln(ui)

is the core efficiency or average

efficiency for each bank which is

time-independent while random error

tends to average out over time. In

order to be consistent with this error

term specification, the cost function

can then be expressed with a residual

in the multiplicative form:

Costi,t = Ct(Qi,t,Pi,t)vi,t,ui,

where Ct is

a cost function and Qi,t

and Pi,t are

output and input prices, respectively.

This cost function in logarithm is:

1nCosti,t =

1nCt(Qi,t,Pi,t)

+ 1n(vi,t) +

1n(ui).

The term 1n(ui)

is assumed to be orthogonal to the

regressors in the cost function. The

error term  i,t

can be estimated for each bank for

each year. In this way the parameters

in the cost function and the random

error term 1n(vi,t)

are allowed to change for each year

while 1n(ui)

remains constant over time. i,t

can be estimated for each bank for

each year. In this way the parameters

in the cost function and the random

error term 1n(vi,t)

are allowed to change for each year

while 1n(ui)

remains constant over time.

The next step is to average the estimated

cost function, error term i,t

for each bank over n years in order

to obtain an estimate of 1n(ui),

that is 1n(ui)

=

For each bank then the percentage

efficiency measure can be expressed

as:

EFFi = exp[1n(umin)

– 1n(ui)],

where 1n(umin)

is the minimum value of 1n(ui).

From this formulation an efficiency

value of 1 corresponds to the most

efficient bank while all other banks

have values between 1 and 0.

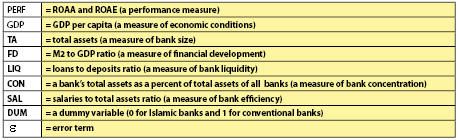

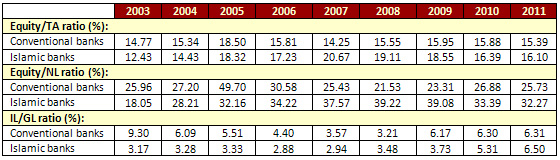

Factors Affecting Bank Performance

Profitability is one of the widely

used indicators to measure the performance

of any business. Financial ratios

used in this study for measuring a

bank's profitability are: return on

average assets (ROAA), return on average

equity (ROAE), and cost to income

(C/I) ratio. For ROAA and ROAE, the

higher the ratio, the better is the

bank's performance. For cost to income

ratio, the lower the ratio, the better

is the bank's performance.

Maintaining adequate liquidity is

one of the major challenges that banks

face. Liquidity ratios measure a bank's

ability to meet its short-term obligations.

In this study three liquidity ratios

are used: net loans to total assets

(NL/TA) ratio, liquid assets to customer

deposits and short-term funding (LA/DSF)

ratio, and net loans to total deposits

and borrowings (NL/TDB) ratio. The

higher the NL/TA ratio, the lower

is the bank's liquidity. The higher

the LA/DSF ratio, the more liquid

is the bank. The higher the NL/TDB

ratio, the higher is the chance that

the bank faces liquidity risk.

Solvency is the ability of a bank

to have enough assets to cover its

liabilities. A bank is insolvent if

its equity is negative. The first

ratio used to gauge solvency is equity

to total assets (E/TA) ratio. The

higher the E/TA ratio, the larger

is the bank's capacity to absorb loan

losses. The second ratio used is equity

to net loans (E/NL) ratio. The higher

the E/NL ratio, the larger is the

bank's capacity to absorb loan losses.

The third ratio used is impaired loans

to gross loans (IL/GL) ratio. The

lower the IL/GL ratio, the better

is the bank's credit quality and the

lower is its loan losses.

To examine factors affecting bank

performance, the following multiple

regression model is used:

PERF = b0 +

b1GDP + b2TA

+ b3FD + b4LIQ

+ b5CON + b6SAL

+

where

Two controlled variables are used

in the regression model. Since larger

banks might have enjoyed scale or

scope economies that had positive

effects on their performance, the

size of banks in terms of assets (scale)

is used to control for bank size.

In addition, as business cycle might

also affect bank performance, GDP

per capita is used to control for

macroeconomic conditions.

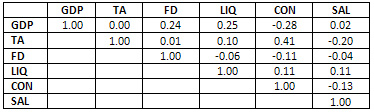

Before running the regression, a multicollinearity

test is used to examine the degree

of correlation among the explanatory

variables. Table 4 shows the pairwise

correlations. As the highest correlation

is only 0.41, the explanatory variables

are not multicollinear.

Table 4: Correlation Coefficients

of Explanatory Variables

Data

The sample consists of 58 GCC conventional

and Islamic banks listed in the respective

stock exchanges during the 2003-2011

period. All the required data are

extracted from the annual reports

of the banks and the Statistical Bulletin

of the central banks.

Empirical findings

To explore bank efficiency, the panel

data for all national banks that operated

throughout the whole study period

is used. The DFA approach is employed

to calculate the efficiency scores

of the banks. As shown in Table 5,

Masraf Al Rayan of Qatar was the most

efficient bank while Kuwait Finance

House was the least efficient bank

during the study period. It is interesting

to note that both are Islamic banks.

Table 5: Efficiency of Islamic

Banks, 2003-2011

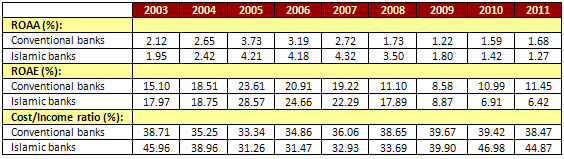

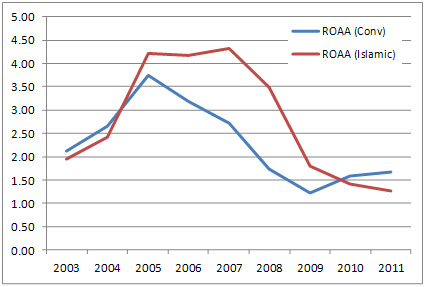

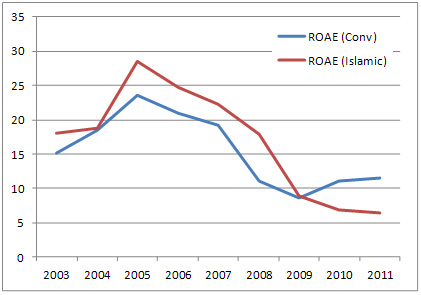

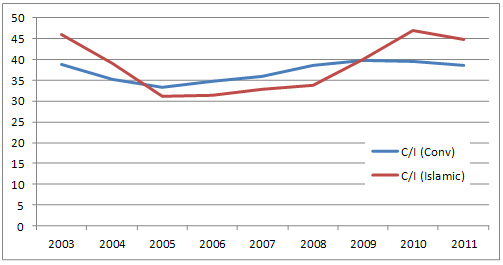

Table 6 and Figures 1-3 show the profitability

ratios of conventional and Islamic

banks between 2003 and 2011. In general,

all three ratios indicate that Islamic

banks were more profitable than conventional

banks during the 2005-2009 period.

Table 6: Profitability Ratios of Conventional

versus Islamic Banks

Figure 1: Return on Average Assets

(ROAA) of Conventional versus Islamic

Banks

Figure 2: Return on Average Equity

(ROAE) of Conventional versus Islamic

Banks

Figure 3: Cost to Income (C/I)

Ratio of Conventional versus Islamic

Banks

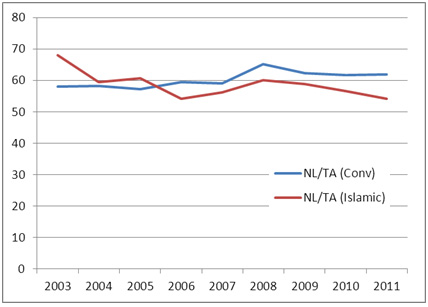

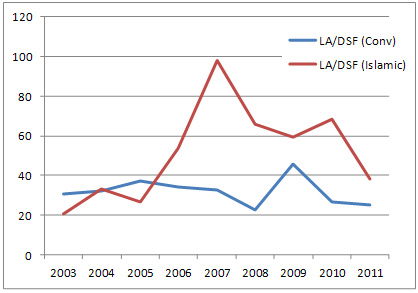

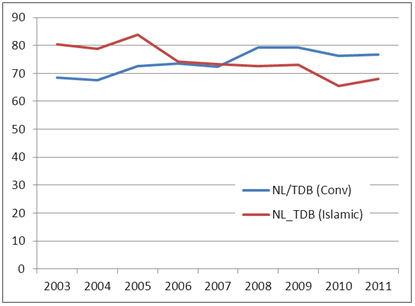

Table 7 and Figures 4-6 present the

liquidity ratios of conventional and

Islamic banks between 2003 and 2011.

In general, all three ratios reveal

that Islamic banks were more liquid

than conventional banks for the 2006-2011

period.

Table 7: Liquidity Ratios of Conventional

versus Islamic Banks

Figure 4: Net Loans to Total Assets

(NL/TA) Ratio of Conventional versus

Islamic Banks

Figure 5: Liquid Assets to Deposits

and Short Term Funding (LA/DSF) Ratio

of Conventional versus Islamic Banks

Figure 6: Net Loans to Total Deposits

Borrowings (NL/TDB) Ratio of Conventional

versus Islamic Banks

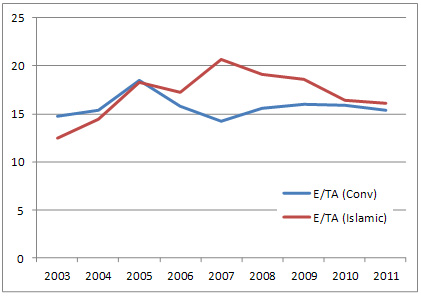

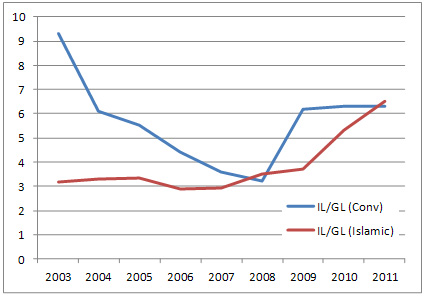

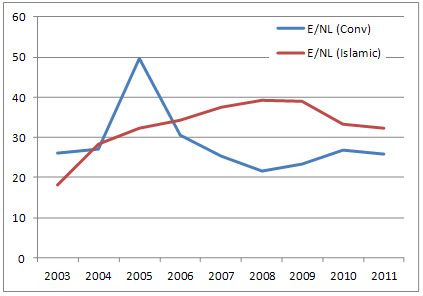

Table 8 and Figures 7-9 display the

solvency ratios of conventional and

Islamic banks between 2003 and 2011.

In general, all three ratios indicate

that Islamic banks were more solvent

than conventional banks during the

2006-2011 period.

Table 8: Solvency Ratios of Conventional

versus Islamic Banks

Figure 7: Equity to Total Assets

(E/TA) Ratio of Conventional versus

Islamic Banks

Figure 8: Impaired Loans to Gross Loans

(IL/GL) Ratio of Conventional versus

Islamic Banks

Figure 9: Equity to Net Loans Ratio

(E/NL) of Conventional versus Islamic

Banks

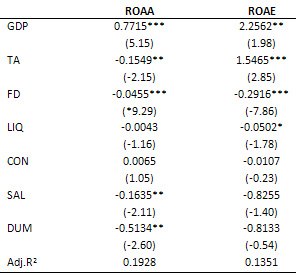

Table 9 presents the results for

the two regression models using return

on average assets (ROAA) and return

on average equity (ROAE) as the dependent

variable. The regression results are

better when ROAA is used as the dependent

variable. GDP per capita, total assets,

M2 to GDP, salaries to total assets,

and type of bank (conventional or

Islamic) are significant variables

affecting ROAA.

Table 9: Regression Results

* Significant at 10% level.

** Significant at 5% level.

*** Significant at 1% level.

Conclusion

In this study, we used a sample of

58 publicly listed GCC national banks

to examine the efficiency and performance

of the GCC banking sector between

2003 and 2011. The results indicate

that Masraf Al Rayan of Qatar was

the most efficient bank (an Islamic

bank) while Kuwait Finance House (also

an Islamic bank) was the least efficient

bank. Conventional banks were more

profitable, liquid, and solvent than

Islamic banks during the earlier years

of the study period whereas Islamic

banks were more profitable, liquid,

and solvent than conventional banks

during the later years of the study

period. Regression results indicate

that economic conditions, bank size,

financial development, operating costs,

and the type of bank (conventional

versus Islamic) are significant variables

affecting ROAA.

References

Al-Tamimi, H. 2010. Factors influencing

performance of the UAE Islamic and

conventional national bank. Global

Journal of Business Research, 4 (2):

1-9.

Berger, A. 1993. Distribution-free

estimates of efficiency in the U.S.

banking industry and tests of the

standard assumptions. Journal of Productivity

Analysis, 4: 261-292.

Chang, T., & Chiu, Y. 2006. Affecting

factors on risk-adjusted efficiency

in Taiwan's banking industry. Contemporary

Economic Policy, 24 (4): 634-648.

Fitzpatrick, T., & McQuinn , K.

2005. Cost efficiency of UK and Irish

Credit Institutions. The Economic

and Social Review, 36 (1): 45-66.

Fayed, M. 2013. Comparative performance

study of conventional and Islamic

banking in Egypt. Journal of Applied

Finance & Banking, 3 (2): 1-14.

Hanif, M., Tariq, M., Tahir, A., &

Momeneen, W. 2012. Comparative performance

study of conventional and Islamic

banking in Pakistan. International

Research Journal of Finance and Economics,

83: 62-72.

Hunter W., & Timme, S. 1995. Core

deposits and physical capital: A reexamination

of bank scale economies and efficiency

with quasi-fixed input. Journal of

Money, Credit, and Banking, 27 (1):

165-185.

Ika, S., & Abdullah, N. 2011.

A comparative study of financial performance

of Islamic banks and conventional

banks in Indonesia. International

Journal of Business and Social Science,

2 (15): 199-207.

Inui, T., Park, J., & Shin, H.

2008. International comparison of

Japanese and Korean banking efficiency.

Seoul Journal of Economics, 21( 1):

195-227.

Jaffar M., & Manarvi, I. 2011.

Performance comparison of Islamic

and conventional banks in Pakistan.

Global Journal of Management and Business

Research, 11 (1).

Matousek, P., & Taci, A. 2004.

Efficiency in banking: Empirical evidence

from the Czech Republic. Economics

of Planning, 37( 2): 225-244.

Ozkan-Gunay E. & . Tektas, A.

2006. Efficiency analysis of the Turkish

banking sector in precrisis and crisis

period: a DEA approach. Contemporary

Economic Policy, 24 (3): 418-431.

Pruteanu-Podpiera, A., Weill, L.,

& Schobert, F. 2008. Banking competition

and efficiency: A micro-data analysis

on the Czech banking industry. Comparative

Economic Studies, 50 (2): 253-273.

Sehrish, S., Saleem, F.,Yasir, M.,

Shehzad, F., & Ahmed, K. 2012.

Financial performance analysis of

Islamic banks and conventional banks

in Pakistan: A comparative study.

Interdisciplinary Journal of Contemporary

Research in Business, 4 (5): 186-200.

Usman, A., & Khan, M. 2012. Evaluating

the financial performance of Islamic

and conventional banks of Pakistan:

A comparative analysis. International

Journal of Business and Social Science,

3 (7), 253-257.

Wu, H., Chen, C., & Shiu, F. 2007.

The impact of financial development

and bank characteristics on the operational

performance of commercial banks in

the Chinese transitional economy.

Journal of Economic Studies, 34 (5):

401-414.

|